The financial technology sector has transitioned from a phase of disruptive experimentation to becoming the structural backbone of the global economy. While the early days of fintech were defined by consumer-facing apps and basic digital banking interfaces, the current environment is characterized by deep infrastructure changes, regulatory maturity, and the integration of advanced artificial intelligence. To evaluate profitability, scalability, and the capacity to negotiate complicated regulatory settings in a world with high interest rates, investors and industry experts are now going beyond user acquisition figures.

Instead of slowing the sector’s growth, this maturity transition has focused resources on technologies that provide measurable efficiency and utility. By 2026, a hybrid financial ecosystem will have emerged from the integration of traditional banking protocols, decentralized finance, and AI-driven automation. This development is changing how companies handle liquidity, how customers obtain credit, and how money flows internationally. The most important factors currently changing the industry are represented by the following trends.

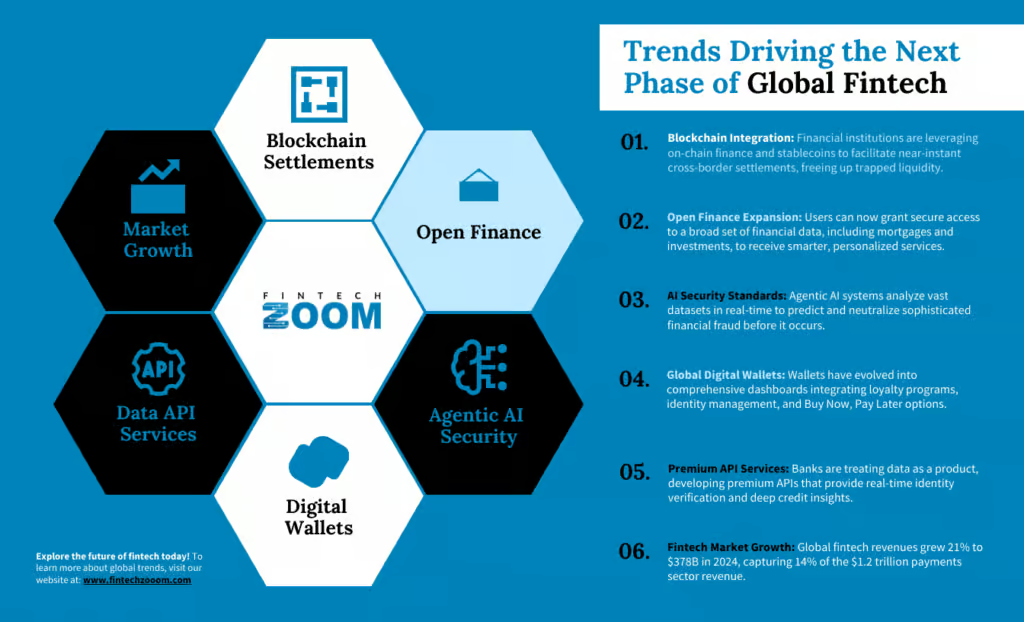

Blockchain Integration Accelerating Cross-Border Settlements

The narrative surrounding blockchain technology has decisively changed from speculative asset trading to institutional utility, specifically with cross-border payments. For years, international settlements were plagued by slow processing times, high intermediary fees, and a lack of transparency.

Some digital industries were early adopters of these technologies. Online gaming platforms, like offshore casinos, integrated cryptocurrency deposits and withdrawals early on. Using Bitcoin, Ethereum, or Dogecoin, for example, allowed users from different regions to move funds quickly at a fraction of the cost without waiting for international banking transfers to clear (source: gamblinginsider.com). For globally distributed user bases, blockchain payments offered a practical solution to delays and high processing costs.

In the freelance economy, various platforms began using blockchain rails to help international freelancers receive payments faster, often settling transactions in hours rather than days, which is very important too not fail at costumer discovery. By bypassing traditional banking intermediaries, these systems reduce friction for cross-border payments and provide greater transparency for both businesses and workers.

Today, financial institutions are leveraging on-chain finance, including stablecoins and asset tokenization, to facilitate near-instant settlements. This technological leap allows businesses to free up trapped liquidity that would otherwise sit in correspondent banking accounts for days, optimizing working capital in an increasingly volatile global market.

This efficiency is driving substantial economic growth within the sector, proving that the underlying technology has value far beyond volatile cryptocurrency markets. Global fintech revenues grew 21% in 2024 to $378 billion, outpacing the broader financial services sector’s 6% growth. This disparity shows how blockchain-integrated fintech solutions are capturing market share from legacy institutions that have been slower to modernize their banking infrastructure. As regulatory frameworks like Europe’s MiCA provide clearer guidelines, we are seeing a surge in mainstream adoption of these blockchain-based payment rails.

Open Finance & Data Commercialization

One of the most significant developments influencing fintech is the expansion of open banking into full-scale open finance ecosystems. Early open banking frameworks mainly focused on payment accounts, allowing consumers to share transaction data with third-party apps. The next phase goes much further.

Open finance allows users to grant secure access to a much broader set of financial information, including mortgages, retirement accounts, insurance policies, and investment portfolios. The goal is to create a more complete financial picture that applications can use to deliver smarter, more personalized services.

At the same time, financial institutions are beginning to treat their data infrastructure as a commercial product. In the past, data-sharing systems were largely built to comply with regulatory mandates such as open banking rules.

Today, many banks are developing premium application programming interfaces (APIs) that provide improved capabilities beyond the standard data feeds required by regulation. These services can include real-time identity verification tools, deeper historical transaction data, or advanced credit insights based on long-term financial behavior.

This created a new value chain within fintech. Banks act as data providers, fintech platforms build applications on top of that information, and consumers gain access to highly personalized financial tools. Open finance is transforming raw financial data into a new digital asset that powers everything from automated savings optimization to comprehensive “financial health” dashboards.

Artificial Intelligence Improving Financial Security Standards

Artificial intelligence has advanced past simple chatbots to become the direct defense mechanism against increasingly sophisticated financial fraud. The rise of “agentic AI”, autonomous systems capable of making decisions and taking actions without human intervention, is significantly changing how institutions detect and neutralize threats.

These systems can analyze vast datasets in real-time to identify irregular transaction patterns that would be invisible to human analysts or rule-based legacy systems. By predicting fraudulent behavior before it occurs, fintechs are significantly reducing chargeback rates and false positives, which have historically been a major friction point for digital commerce.

The capital flowing into the sector reflects the high priority investors place on these AI-driven security and efficiency enhancements. US fintech investment reached $25.1 billion in 2025 across 2,449 deals, representing a 13% increase from 2024 and maintaining the US as the leading market.

A significant portion of this funding is directed toward companies developing proprietary AI models for identity verification and anti-money laundering (AML) compliance. As financial crime becomes more automated, the industry’s reliance on AI for security standards is becoming absolute, creating a competitive moat for firms that can deploy the most advanced defensive algorithms.

Digital Wallet Adoption Is Expanding Globally

The dominance of digital wallets represents the final blow to the era of physical plastic cards and cash. Digital wallets have evolved from simple payment storage tools into comprehensive financial dashboards that integrate loyalty programs, identity management, and “Buy Now, Pay Later” (BNPL) options directly at the point of sale.

This consolidation of services enhances user retention and provides merchants with valuable data insights that standalone credit card transactions never could. The convenience of tapping a phone or smartwatch has fundamentally altered consumer behavior, making the digital wallet the main interface for daily economic interaction.

This behavioral change has allowed fintech companies to capture a significant slice of the global payments revenue pie. Fintechs captured 14% of the $1.2 trillion payments sector revenues in 2024, driven by digital wallets and SaaS-based infrastructure. As these platforms become “super apps,” the differencebetween a payment method and a lifestyle management tool will continue to blur, solidifying fintech’s role as the central operator of daily life.