Imagine a scenario where you face an unexpected yet substantial expense. It could be a significant home repair or a once-in-a-lifetime opportunity for a dream vacation. You have two options: a personal loan or a buy now, pay later (BNPL) option. This scenario encapsulates a familiar financial crossroads faced by today’s consumers.

The current financial landscape oscillates between the need for disciplined budgeting and the temptation of instant acquisition amid rising household debt. It’s no longer surprising if you, as an astute borrower, want to know more about personal loans and BNPL schemes.

What are personal loans?

Personal loans are unsecured debt usable for various purposes. These loans do not require collateral and depend on the borrower’s creditworthiness. They have fixed interest rates, which provide predictability in repayments. As such, they have defined repayment periods that offer a clear timeline for debt clearance.

Personal loans can significantly impact the borrower’s credit score, making responsible borrowing and timely repayments crucial.

Despite their benefits, personal loans can be costly in the long run due to interest accrual. Even with fixed rates, the interest over the life of the loan can add a significant amount to the total repayment sum.

The impact on credit scores is another concern. While responsible use of personal loans can improve a credit score, missed payments or overleveraging can lead to negative consequences. This risk makes it imperative for borrowers to assess their repayment capability before taking out a personal loan.

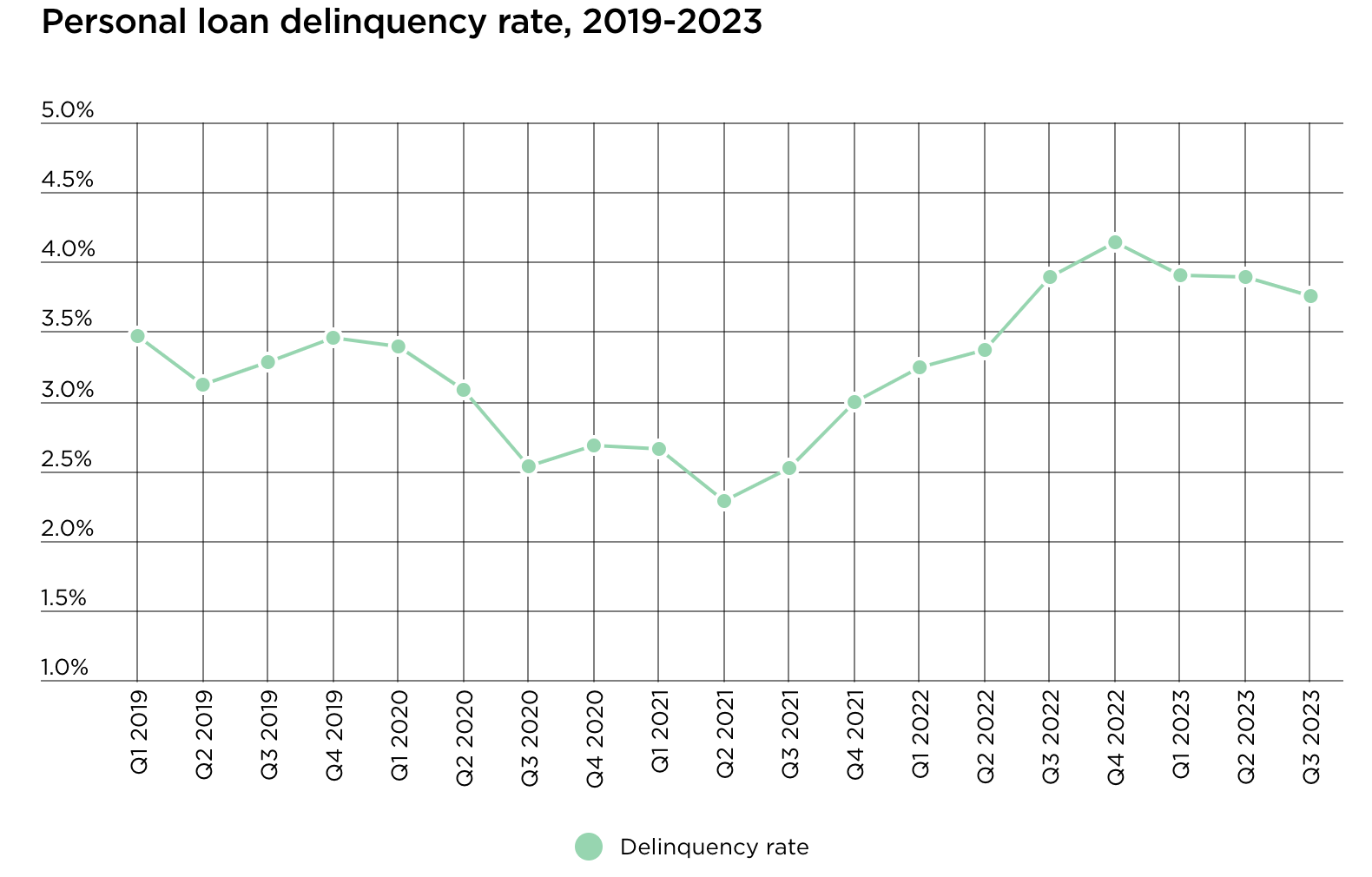

The personal loan debt amount in the US has consistently increased over recent years, apart from a slight dip in 2020. Data reveals that as of the Q3 of 2023, about 3.75 percent of personal loan holders were 60 days overdue.

What’s a good reason to get a personal loan?

Here are some scenarios where a personal loan for debt consolidation can be beneficial:

Consolidating credit card debts: A personal loan can pay off several credit card balances with high interest rates. Personal loans often come with a lower interest rate compared to credit cards.

Combining various debts for simplicity: Different payments and due dates can be overwhelming if you have multiple debts like a car loan and a medical bill. A personal loan can combine these debts into one monthly payment.

Lowering overall interest rates: Imagine you have high debt rates, such as retail store cards or high-interest personal loans. If you can obtain a lower-interest consolidation loan, you will reduce the interest over the life of the loan. This option not only saves money but can also allow you to settle the principal balance quickly.

What is buy now, pay later?

Buy now, pay later schemes have revolutionized retail and online shopping, allowing consumers to spread out payments. Typically, these schemes involve splitting the cost of a purchase into smaller, often interest-free payments, payable over weeks or months. This accessibility and flexibility have made BNPL popular among younger consumers and those looking to manage cash flow effectively.

BNPL’s popularity, which accounts for five percent of global e-commerce sales, can be due to the minimal eligibility requirements. The absence of a traditional credit check for most BNPL plans makes them accessible to a broader audience, even to those with limited or no credit history.

However, BNPL has its pitfalls. Late fees on missed payments can be substantial, and the ease of obtaining multiple BNPL plans can lead to overspending. Managing several different repayment schedules can be challenging and, if not handled properly, can result in financial strain and debt accumulation.

BNPL plans typically do not contribute to building a credit history. This lack of credit-building opportunity can be a significant downside for individuals looking to establish or improve their credit scores.

What’s a good reason to get BNPL?

Here are some scenarios where BNPL can be particularly advantageous:

Taking advantage of a sale or limited-time offer: Say a significant discount or limited-time offer is available on an item you plan to buy. Using BNPL can help you capitalize on the savings opportunity without paying the entire cost upfront.

Testing a product before full commitment: BNPL is a good option if you’re uncertain about a product. With it, you can try the product first. If it doesn’t meet your expectations, you can return it without committing the total amount upfront.

Budgeting for special occasions: For special events like holiday shopping or buying gifts, BNPL can help you manage these expenses without disrupting your regular budget. Spreading the cost over a few months can ease the financial pressure typically associated with such occasions.

Personal Loans vs. Buy Now, Pay Later: Differences

The primary differences between personal loans and buy now, pay later schemes lie in various aspects such as loan amounts, use of funds, convenience, fees, interest charges, and repayment terms. Let’s discuss them in detail:

Loan amounts: Personal loans typically offer higher borrowing limits than BNPL schemes. They are suitable for more significant expenses like home renovations or debt consolidation. BNPL, on the other hand, is generally used for smaller, consumer-level purchases.

Use of funds: Personal loans offer more flexibility regarding the use of funds. They can be used for almost any purpose, from funding large expenses to consolidating debts. BNPL is usually tied to specific purchases at retailers and is limited to the item’s cost.

Convenience: BNPL is often perceived as more convenient for immediate purchases. It has a simple, quick approval process integrated into the checkout experience. Personal loans involve a more comprehensive application process, including credit checks and potentially longer approval times.

Fees and interest charges: Personal loans usually come with interest rates and sometimes origination fees, often lower than credit card interest rates. BNPL schemes often advertise zero interest, but late fees can be substantial, and some plans may have hidden costs.

Repayment terms: Personal loans have longer repayment periods, typically from a year to several years. BNPL plans offer shorter repayment schedules, usually weeks to a few months.

When choosing between these options, consider:

- Financial goals and credit-building: Personal loans can help build credit if repaid responsibly, as activity is typically reported to credit bureaus. BNPL might not always aid in building credit, as not all providers report to credit bureaus.

- Purchase size and repayment capacity: A personal loan may be more suitable for larger, long-term expenses. BNPL is better for smaller purchases you can pay quickly.

- Interest rates and total cost of financing: Evaluate the total cost over time, including interest rates for personal loans and potential fees for BNPL plans. The longer repayment term of a personal loan might mean paying more interest over time despite a lower annual rate. To date, interest rates for personal loans fall between 4 to 36 percent.

Personal Loans or Buy Now, Pay Later: Which is for you?

The decision between a personal loan and a BNPL scheme hinges on your financial needs, goals, and circumstances. Personal loans are typically more suitable for larger, long-term financial commitments. They offer the flexibility of use and lower overall interest costs for extended credit.

BNPL, conversely, caters to immediate, smaller purchases, providing a convenient and often interest-free short-term financing solution. However, it’s less likely to impact your credit score positively and can come with hefty fees if you miss payments.

Ultimately, the key is to decide based on a thorough assessment of your financial situation. Consider the total cost of the loan, how it fits into your budget, and how it aligns with your financial goals. The most important factor is managing the repayments responsibly to avoid financial strain and maintain a healthy financial profile.

References:

- https://www.chime.com/blog/personal-loans-vs-buy-now-pay-later/

- https://www.nerdwallet.com/article/loans/personal-loans/use-of-buy-now-pay-later-outpaces-personal-loans-in-past-year

- https://www.amone.com/blog/personal-loans-vs-buy-now-pay-later/

- https://www.nerdwallet.com/article/loans/personal-loans/buy-now-pay-later

- https://www.experian.com/blogs/ask-experian/personal-loans-vs-buy-now-pay-later/